What is Section 138? Everything You Need to Know

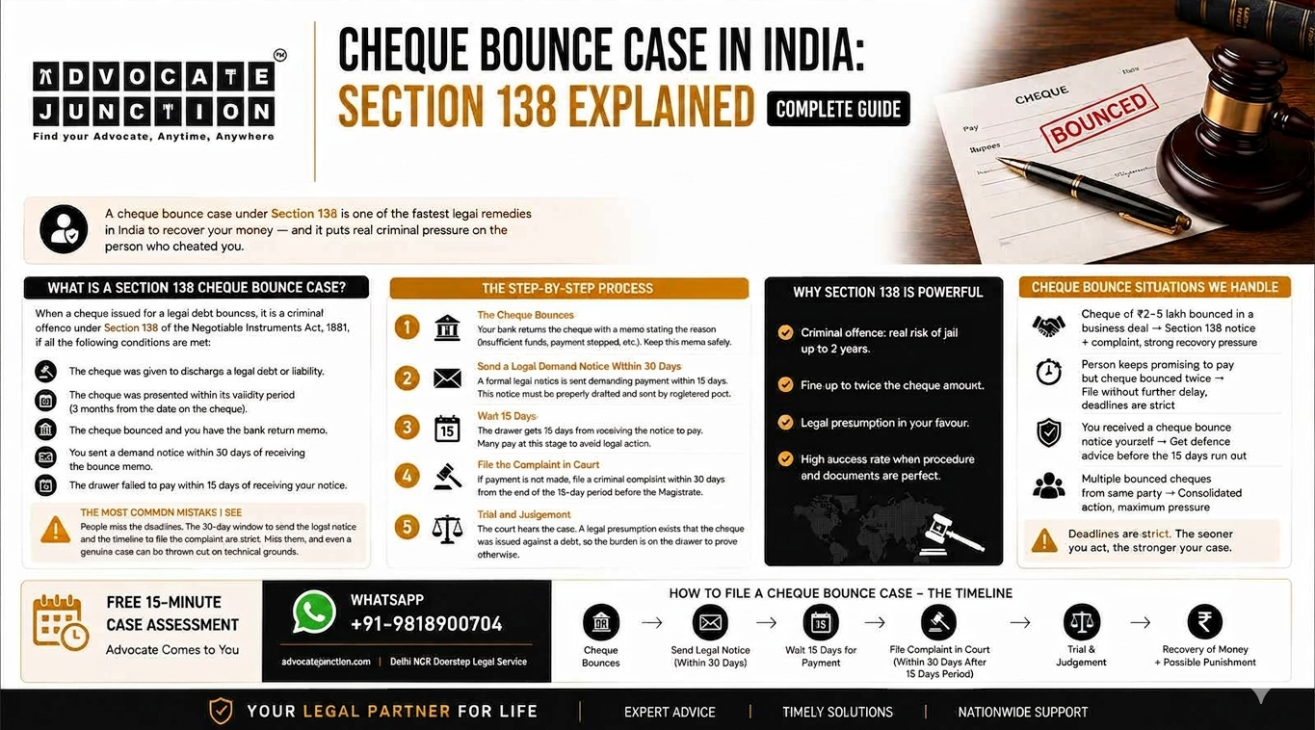

A Cheque Bounce case under Section 138 is one of the fastest legal remedies in India to recover your money — and it puts real criminal pressure on the person who cheated you.

Jail or Just a Fine? The Real Consequences of a Bounced Cheque

When someone walks in holding a bounced cheque, the first question is almost always the same: “Will I actually get my money back — and can this person go to jail?”

The honest answer is yes to both, potentially. A cheque bounce case under Section 138 of the Negotiable Instruments Act is unusual in Indian law because it is a criminal remedy for what is essentially a money matter. That criminal element — the real possibility of a fine up to twice the cheque amount, or imprisonment up to two years — is exactly what makes defaulters pay up, often before the case even concludes.

Let me walk you through the whole thing the way I would explain it across my desk.

What Exactly is a Section 138 Cheque Bounce Case?

When someone gives you a cheque and it bounces — for insufficient funds, or because they stopped payment, or the account was closed — that is not just a broken promise. Under Section 138 of the Negotiable Instruments Act 1881, it is a criminal offence, provided certain conditions are met.

For a valid Section 138 case, these must all be true:

- The cheque was given to discharge a legal debt or liability — not as a gift or loan security without an underlying debt.

- The cheque was presented to the bank within its validity period — three months from the date on the cheque.

- The cheque bounced — the bank returned it unpaid, and you have the cheque return memo.

- You sent a demand notice within 30 days of receiving the bounce memo.

- The drawer failed to pay within 15 days of receiving your notice.

| The most common mistake I see

People miss the deadlines. The 30-day window to send the legal notice after the cheque bounces, and the timeline to file the complaint after that, are strict. Miss them, and even a genuine case can be thrown out on technical grounds. This is exactly why getting a lawyer involved the moment a cheque bounces matters so much. |

The Step-by-Step Process

Step 1 — The Cheque Bounces

Your bank returns the cheque with a memo stating the reason — usually ‘insufficient funds’ or ‘payment stopped by drawer’. Keep this return memo safely. It is the foundation of your entire case, proof of the date the cheque was dishonored.

Step 2 — Send a Legal Demand Notice Within 30 Days

This is the most time-sensitive step. Within 30 days of the bounce, your advocate sends a formal legal notice to the person who gave the cheque, demanding payment of the cheque amount within 15 days. This notice must be properly drafted and sent by registered post — its wording and timing are critical.

Step 3 — Wait 15 Days

The drawer gets 15 days from receiving the notice to pay. Many pay at this stage — the arrival of a formal legal notice, and the realization that a criminal case is coming, is often enough. If they pay, your matter is resolved. If they do not, you move to court.

Step 4 — File the Complaint in Court

If payment is not made within 15 days, you have 30 days from the end of that period to file a criminal complaint before the Magistrate. Your advocate files it with the bounced cheque, the return memo, the legal notice, and proof of its delivery. The court then issues summons to the drawer.

Step 5 — Trial and Judgement

The case proceeds. Because a bounced cheque carries a legal presumption that it was issued against a debt, the burden is largely on the drawer to prove otherwise. This makes Section 138 cases relatively favorable for the person holding the cheque, provided the paperwork is clean.

| Cheque Bounce Situations We Handle

Real matters at Patiala House and Delhi NCR courts — 2026 |

| Cheque of ₹2–5 lakh bounced in a business deal → Section 138 notice + complaint, strong recovery pressure |

| Person keeps promising to pay but cheque bounced twice → File without further delay, deadlines are strict |

| You received a cheque bounce notice yourself → Get defence advice before the 15 days run out |

| Multiple bounced cheques from same party → Consolidated action, maximum pressure |

| Deadlines are strict. The sooner you act, the stronger your case.

FREE 15-Minute Case Assessment — Advocate Comes to You WhatsApp: +91-9818900704 advocatejunction.com | Delhi NCR Doorstep Legal Service |

What Can You Recover — and the Jail Question

On conviction under Section 138, the court can impose a fine of up to twice the cheque amount, or imprisonment up to two years, or both. In practice, courts most often order the defaulter to pay compensation — frequently the full cheque amount plus costs — and the threat of imprisonment is the lever that secures payment.

So when a client asks “can they go to jail” — yes, that is a real possibility, and it is precisely why Section 138 works. Most defaulters would rather pay than risk a criminal conviction and jail.

| Dashrath Rupsingh Rathod v. State of Maharashtra | 2014 | Supreme Court of India

An important judgement on the question of jurisdiction — where a cheque bounce case can be filed. The law was later amended, but this case shaped how territorial jurisdiction is understood in Section 138 matters. Your advocate uses the current position to file in the most convenient and valid court for you. |

| Meters and Instruments Pvt Ltd v. Kanchan Mehta | 2017 | Supreme Court of India

The Supreme Court dealt with the compounding and quick disposal of cheque bounce cases, encouraging settlement and treating these matters as primarily about recovering the money owed. Useful when your goal is fast payment rather than a prolonged fight. |

Frequently Asked Questions

How long does a cheque bounce case take?

Cheque bounce cases are meant to be dealt with faster than ordinary criminal matters, and courts are encouraged to dispose of them quickly. In practice a case may take several months to a couple of years depending on the court and whether the accused contests. But remember — many defaulters pay after the legal notice or early in the proceedings, so you often recover well before final judgement.

The cheque was given as security, not for a debt. Is it still a 138 case?

This is a common defense. Section 138 applies when the cheque was issued for a legally enforceable debt or liability. If a cheque was genuinely given only as security with no underlying debt, that is a defense the drawer can raise. But there is a legal presumption in favor of the holder, so the drawer must prove it. These situations turn on facts and documents — get specific advice.

I lost the bounce memo. Can I still file?

The bank can issue you a duplicate return memo. It is important evidence, so obtain a copy from your bank. Do not let a lost memo stop you — but act quickly, because the deadlines run from the date of dishonor regardless.

Can I also file a civil case to recover the money?

Yes. Section 138 is a criminal remedy, but you can also pursue a civil recovery suit or a summary suit for the money. Often the criminal case alone secures payment because of the jail risk, but in larger matters both routes can be pursued. Your advocate will advise the best combination for your case.

Do Not Wait — the Clock is Already Running

The single most important thing about a cheque bounce case is timing. The 30-day notice window, the 15-day payment period, the 30-day filing window — these deadlines are strict, and missing them can sink a genuine claim. The day a cheque bounces, the clock starts.

At AdvocateJunction, we handle cheque bounce cases across Delhi NCR — from the legal notice through to recovery. We come to you, review your cheque and memo, and move fast to protect your deadlines. The first 15 minutes are free.

WhatsApp us at +91-9818900704 the day your cheque bounces.

Related Articles on this topic

- Is Cheque Bounce a Criminal Offence in India?

- NRI Cheque Bounce Cases Complete Guide.

- Five biggest mistakes in Cheque Bounce Cases.

- Rajpal Yadav Cheque Bounce Case

- Amisha Patel Cheque Bounce Case

© 2026 AdvocateJunction. All rights reserved. | advocatejunction.com | For informational purposes only. Not legal advice