NRI Cheque Bounce Case India: The Complete Legal Guide (2026)

Navigating an NRI cheque bounce case India requires a strategic legal approach, especially when managing financial interests from across the globe. For many Non-Resident Indians, a dishonoured cheque is more than a failed transaction; it is a significant legal hurdle that threatens investments in real estate, business ventures, or personal loans. Under Section 138 of the Negotiable Instruments Act, 1881, these cases are criminal offences, but the path to recovery involves strict procedural nuances and tight statutory deadlines.

Managing financial interests and legal obligations across international borders presents a unique set of challenges for the Indian diaspora. For Non-Resident Indians (NRIs), financial transactions in India—ranging from property investments and business ventures to supporting family—often involve the use of cheques. However, when a cheque is returned unpaid by a bank, it triggers a complex legal process that requires immediate attention and a deep understanding of Indian law.

In India, a “cheque bounce” is not merely a breach of trust or a civil matter; it is a criminal offence governed by the Negotiable Instruments Act, 1881 (NI Act). This guide provides an exhaustive roadmap for NRIs to navigate the legalities of Section 138 of the NI Act, manage litigation remotely, and ensure the recovery of their funds.

1. The Legal Foundation: Section 138 of the NI Act

“When dealing with an NRI cheque bounce case India, the first step is understanding the legal foundation of Section 138 of the Negotiable Instruments Act. This provision was designed to enhance the credibility of cheques and ensure that business transactions are not stalled by the issuance of hollow promises.

For a cheque bounce to qualify as a criminal offence under this section, four essential criteria must be satisfied:

-

The Existence of a Debt: The cheque must have been issued for the discharge, in whole or in part, of any legally enforceable debt or other liability. A cheque given as a gift, donation, or for an illegal purpose does not attract criminal liability.

-

Presentation within Validity: The cheque must be presented to the bank within a period of three months from the date on which it is drawn, or within the period of its validity, whichever is earlier.

-

Dishour for Specific Reasons: The cheque must be returned by the bank unpaid, either because the amount of money standing to the credit of that account is insufficient to honour the cheque or it exceeds the amount arranged to be paid from that account by an agreement made with the bank.

-

Failure to Pay After Notice: The drawer of the cheque fails to make the payment within 15 days of receiving a formal legal demand notice from the payee.

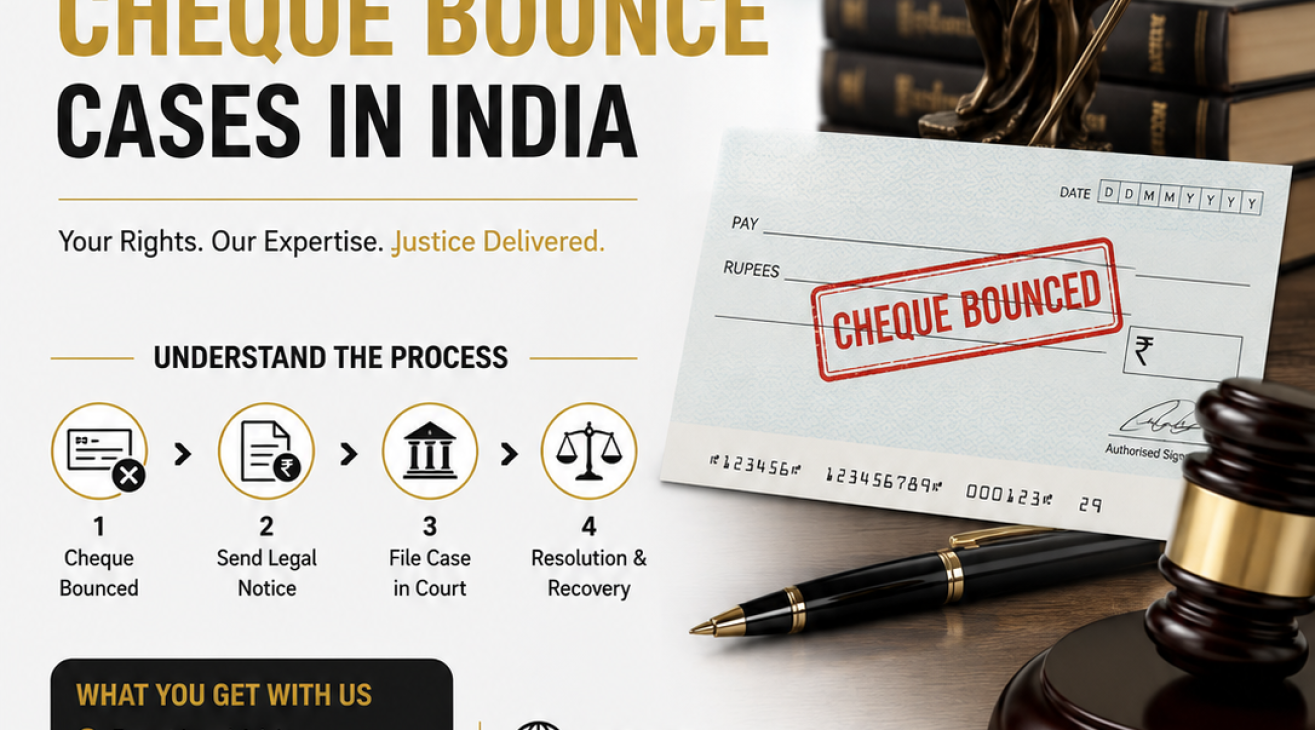

2. The Strict Timeline of a Cheque Bounce Case

The Indian legal system imposes strict “limitation periods” for cheque bounce cases. For an NRI living in a different time zone, monitoring these dates is the most critical aspect of the case. Missing a deadline can result in the loss of the right to file a criminal complaint.

Phase 1: The Return Memo

When a bank refuses to process a cheque, it issues a “Cheque Return Memo” to the person who deposited it. This document contains the date of dishonour and the specific reason (e.g., “Insufficient Funds,” “Account Closed,” or “Refer to Drawer”). The 30-day countdown for the next step begins the moment you or your representative receives this memo.

Phase 2: The Statutory Legal Notice

Within 30 days of receiving the Return Memo, you must send a formal legal notice to the person who issued the cheque (the drawer). This notice is a mandatory requirement. It must clearly state the cheque details, the fact that it was dishonoured, and a demand for the payment of the said amount within 15 days from the date the drawer receives the notice.

Phase 3: The Cause of Action

After the notice is successfully delivered, you must wait for 15 days. This is the “grace period” provided by law for the drawer to rectify the situation. If the drawer pays the full amount within these 15 days, the matter ends there. If they fail to pay, the “cause of action” arises on the 16th day.

Phase 4: Filing the Complaint

You have exactly 30 days from the expiry of the 15-day notice period to file a formal criminal complaint in the court of the Judicial Magistrate.

3. Remote Litigation: How NRIs Can Manage Cases

A common misconception is that an NRI must be physically present in India to fight a cheque bounce case. While the law requires participation, there are established mechanisms to handle the bulk of the litigation remotely.

The Special Power of Attorney (SPA)

An NRI can initiate and pursue a Section 138 case through a Special Power of Attorney holder. This person can be a trusted family member, a friend, or your legal counsel in India.

-

The Process: If the PoA is signed outside India, it must be notarized in the country of your residence. Subsequently, it needs to be “apostilled” or attested by the Indian Embassy or Consulate. Once the document reaches India, it must be registered or “adjudicated” at the local SDM (Sub-Divisional Magistrate) office.

-

Competence: The PoA holder must be someone who has personal knowledge of the transaction or has access to the records of the debt. They can sign the complaint, file it in court, and depose during the preliminary evidence stage.

Modern Technology and Virtual Courts

The Indian judiciary has become increasingly digital. Under the current “Video Conferencing Rules,” NRIs can often request the court to record their testimony via video link. This is particularly common during the “cross-examination” phase, where the presence of the complainant is usually required. This significantly reduces the need for international travel.

4. Jurisdiction: Where to File the Case?

Following the 2015 amendment to the NI Act, the rules regarding where a case can be filed were simplified to prevent harassment of the person who received the cheque.

-

If you deposit the cheque in your bank account: The case must be filed in the court that has jurisdiction over the location of the branch of the bank where you maintain your account.

-

If you present the cheque directly at the drawer’s bank: The case is filed where the drawer’s bank branch is located.

For NRIs, this is beneficial. If you maintain an NRE or NRO account in a specific city in India, you can deposit the cheque there and file the case in that city, regardless of where the person who issued the cheque resides.

5. Comparing Legal Remedies: Criminal vs. Civil

While Section 138 is a criminal provision, it is not the only way to recover money. Often, legal experts suggest a multi-pronged approach.

The Criminal Path (Section 138 NI Act)

The primary objective of a criminal case is punishment, which acts as a deterrent. The accused can face imprisonment for up to two years, a fine which may extend to twice the amount of the cheque, or both. Because of the risk of jail time, many accused parties prefer to settle the matter quickly.

The Civil Path (Order 37 of the CPC)

A “Summary Suit” under Order 37 of the Code of Civil Procedure is a faster version of a regular civil suit. Unlike a criminal case, which focuses on punishment, a civil suit focuses purely on the recovery of the money plus interest.

-

Procedure: In a summary suit, the defendant does not have an automatic right to defend the case. They must first apply for “leave to defend,” and if they fail to show a substantial defence, the court can pass a judgement in your favour immediately.

-

Benefit: You can pursue both a criminal case under Section 138 and a civil summary suit simultaneously. One does not bar the other.

6. The 2018 Amendment: Interim Compensation

One of the most powerful tools currently available to NRIs is Section 143A of the NI Act. This amendment was introduced to discourage the accused from using dilatory tactics to delay the trial.

Under this section, the court has the power to order the drawer of the cheque to pay interim compensation to the complainant. This amount can be up to 20% of the cheque value. This order is usually made once the accused pleads “not guilty.” The amount must be paid within 60 days of the court’s order. This ensures that the complainant receives a portion of their money while the trial is still ongoing.

7. Essential Documentation Checklist

For an NRI, documentation is the backbone of the case. Since you are not physically present, your “paper trail” must be impeccable. You will need:

-

The Original Cheque: The court will require the physical cheque, not a photocopy.

-

The Original Bank Return Memo: This is the primary evidence that the bank refused the payment.

-

The Demand Notice and Proof of Service: You must provide the office copy of the notice, the original speed post/registered post receipts, and the “Acknowledgement Due” card or the online tracking report showing “Delivered.”

-

Evidence of Debt: Documents such as loan agreements, invoices, sale deeds, or even email and WhatsApp conversations where the accused acknowledges the debt.

-

Certificate under Section 65B: If you are using digital evidence (like WhatsApp screenshots), you must provide a certificate under Section 65B of the Indian Evidence Act to make it admissible in court.

8. Common Challenges and Strategic Solutions

The “Security Cheque” Defence

The most common defence taken by the accused is that the cheque was given only as “security” for a transaction and was not intended to be encashed. However, Indian courts have repeatedly held that even a security cheque can attract Section 138 liability if a debt was actually due at the time the cheque was presented.

Service of Notice to an NRI

If you are the one who has been issued a notice (i.e., someone claims your cheque bounced), the laws of service are different for those residing abroad. However, for an NRI filing a case, the focus remains on ensuring the accused in India receives the notice at their last known address.

Mediation and Settlement

The Indian judicial system encourages the settlement of cheque bounce cases. Many cases are referred to Lok Adalats or mediation centres. For an NRI, this is often the best route as it leads to a “Compounding of the Offence,” where the case is closed upon the payment of a mutually agreed-upon sum, avoiding years of litigation.

While many NRI-related cases often involve the NRI as the complainant, there are indeed several high-profile cases where an NRI was the issuer of the bounced cheque. Here are two prominent examples .

UK-Based NRI Woman Convicted for Cheque Bounce (2024)

This is a recent and clear-cut case where an NRI woman living in the UK issued a cheque to her neighbour in India that later bounced.

The NRI (Drawer): Nisha Dusra, a UK-based Non-Resident Indian.

The Indian Resident (Payee): Her neighbour in Rajkot, Dhiren Mehta.

· The Incident: In 2015, while visiting her hometown, Dusra told Mehta she was facing technical issues with her UK account and needed help arranging funds. She promised to repay the money in 5-7 days. Mehta arranged ₹9 lakh for her, but when the time came to repay, she issued a cheque that bounced due to insufficient funds in her account.

· Legal Outcome: Mehta sent a legal notice and later filed a case under the Negotiable Instruments Act. The court found Dusra guilty, sentencing her to 15 months of imprisonment and ordering her to pay the cheque amount to the complainant. The court also noted that she was a “habitual criminal” with other cheating cases registered against her in Mumbai.

This case underscores that NRIs are not immune to criminal prosecution in India for cheque bounce offenses, even if they are residing abroad.

Canadian NRI Woman Declared Proclaimed Offender (2009)

This older case illustrates the severe long-term consequences an NRI can face, including being declared an absconder.

· The Parties:

The NRI (Drawer): Balwant Kaur Gill, a Canadian citizen.

The Indian Resident (Payee): Gurmit Singh, a caretaker by profession.

· The Incident: In 2000, following a business deal, Gill handed over a cheque of ₹55 lakh to Singh. The cheque was dishonoured by the bank.· Legal Outcome: The legal proceedings stretched for years. Gill failed to appear in court, presumably having fled to Canada. Consequently, in 2007, a court declared her a proclaimed offender and ordered the attachment of her property in Chandigarh’s Sector 9. However, the case became murky, and the victim continued to struggle for justice years later, partly due to subsequent disputes over the attached property.

This case highlights the challenges an Indian resident can face when an NRI absconds, but it also demonstrates the court’s power to declare a non-resident a proclaimed offender and attach their assets in India.

Summary

These cases demonstrate that the provisions of the Negotiable Instruments Act, 1881, apply equally to NRIs. If a cheque issued by an NRI is dishonoured, a complaint can be filed before a competent Indian court. Physical absence from India does not stop the legal proceedings. NRIs have been sentenced to imprisonment and significant fines, as seen in the first case.

Conclusion

Navigating a cheque bounce case in India as an NRI requires a blend of legal vigilance and strategic planning. By adhering to the strict 30-day timelines, utilizing a Special Power of Attorney effectively, and leveraging modern digital court procedures, NRIs can successfully protect their financial interests without needing to abandon their lives abroad. While the process may seem daunting, the stringent nature of Section 138 provides a robust mechanism to ensure that those who issue dishonoured cheques are held accountable under the law.

Disclaimer – The article is written for information purpose and it is edited by a practising advocate .